The Credit Card Delinquency Crisis: Why Traditional Collections Won't Work in 2026

US credit card delinquency just hit a 15-year high — and the same pressure is building in Canada and the UK. Here's what the data is telling us, and what the card issuers outperforming this market are doing differently.

Key Takeaways

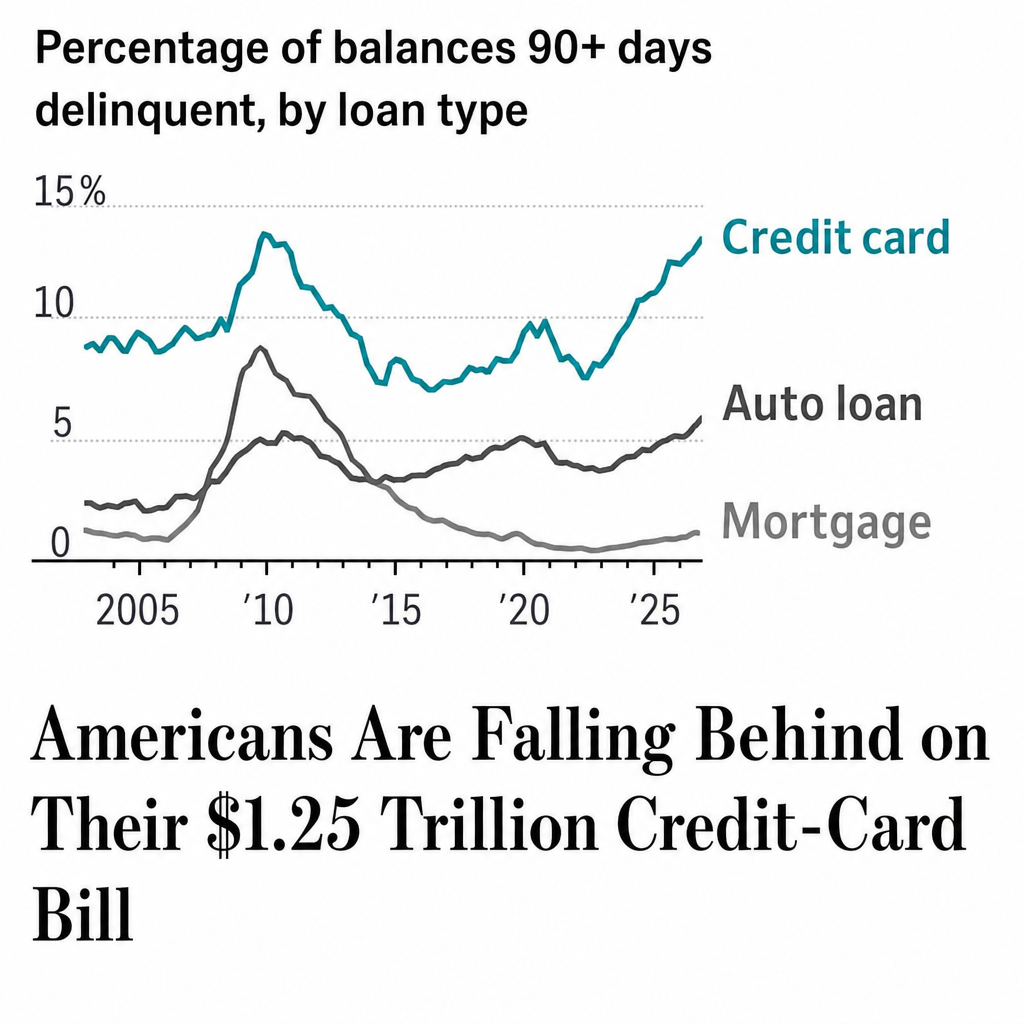

- The share of US credit card balances 90+ days delinquent climbed to 13.12% in Q1 2026 — a 15-year high, the worst since the aftermath of the 2008 financial crisis (New York Fed).

- This is mirrored across borders: Canadian insolvencies hit their highest level since 2009, and UK card accounts with two missed payments rose 14.3% year over year.

- Today's credit card delinquency is an affordability problem, not an awareness problem — and high-frequency, volume-based collections make it worse.

- A leading UK credit card provider achieved a 60% cure rate lift and an 83% reduction in outbound calls using Symend's behavioral Delinquency Archetypes.

- The real opportunity isn't just recovering this wave of delinquency — it's preventing the next one. That's where SymendPrevent changes the equation.

The number every card issuer's leadership team should have front of mind right now: 13.12%.

That's the share of US credit card balances at least 90 days delinquent in the first quarter of 2026, according to the New York Federal Reserve — the highest level in 15 years, and the most since the period following the 2008 financial crisis. It arrives as Americans collectively carry a $1.25 trillion credit card balance, part of a record $18.8 trillion in household debt.

US credit card balances 90+ days delinquent climbed to a 15-year high in Q1 2026. Source: Wall Street Journal, based on New York Federal Reserve data.

This isn't a problem the industry can volume its way out of. The forces driving this wave of delinquency are structural — and the collections playbooks built for an easier market aren't just underperforming. They're actively making recovery harder.

Here's what the data actually shows, why the old approach is failing, and what the issuers winning in this environment are doing instead.

This Is an Affordability Crisis — Across Three Markets

The US headline is alarming on its own, but the more important signal is that the stress is synchronized across developed credit markets. This isn't a local anomaly. It's a consumer affordability squeeze.

United States. Beyond the 13.12% serious-delinquency figure, roughly 4.8% of all outstanding consumer debt is now in some stage of delinquency (New York Fed). Balances aren't falling — credit card debt rose 5.9% year over year — but a growing share of households have less and less margin for error after years of elevated prices and interest rates.

Canada. Equifax Canada's Q1 2026 data tells a strikingly similar story. Total consumer debt reached $2.66 trillion, and consumer insolvency volumes climbed to their highest level since 2009, up 18.8% year over year. More than 1.5 million Canadians missed a credit payment in the prior quarter, with consumers aged 26–35 showing the most acute stress — the same demographic now driving rising credit card delinquency nationally.

United Kingdom. UK card data from FICO shows the share of accounts missing two payments up 14.3% year over year, and a 29.5% month-over-month jump in customers missing one payment during a recurring period of seasonal stress. The percentage of balance customers repay each month has fallen to 33.4%. Separately, Pepper Money found more than 16 million UK adults have experienced some form of adverse credit — the highest in nine years — and notably, the strain has climbed into higher income brackets.

"Three countries, one pattern: balances paid down more slowly, missed payments rising, and stress climbing the income ladder. This is an affordability crisis wearing collections clothing."

When borrowers fall behind under these conditions, it's rarely because they've forgotten the balance exists. It's because the minimum payment is now competing with rent, groceries, and energy bills in a budget that no longer covers all of them. That distinction — between inability to pay and unwillingness to engage — is the single most important thing collections leaders can internalize right now.

Why the Old Playbook Is Making It Worse

Traditional collections was designed for a different kind of delinquency. It assumed most past-due customers just needed a nudge — a call, a letter, a reminder — and that enough outreach would shake the payment loose. That model has three critical failure modes in today's environment.

1. Volume-based outreach assumes awareness, not incapacity

High-frequency contact campaigns are built on the premise that awareness drives action. But for a growing share of today's cardholders, the barrier isn't awareness — it's capacity. Calling the same person twice a day doesn't change a structurally broken budget. It just erodes trust and brand equity, pushing the customer further away at the exact moment you most need them to engage.

2. One-size-fits-all ignores behavioral diversity

A customer who's 30 days past due after a one-time income shock needs a completely different conversation than one who's 30 days past due because they no longer trust the issuer's messaging. Collapsing these into a single workflow doesn't just underperform — it actively pushes salvageable accounts toward charge-off. This is precisely why empathy-driven, personalized engagement consistently outperforms generic pressure.

3. AI without behavioral science is just faster inefficiency

Card issuers are racing to deploy AI in collections — but deploying AI as a higher-throughput version of the same volume-based approach doesn't change the underlying dynamic. As we've argued in the AI collections paradox, generic AI without behavioral intelligence often accelerates the damage rather than reversing it. The market is flooded with AI-only tools that optimize how often you contact someone. The harder and more valuable question is how — and that's a behavioral science problem, not a throughput problem.

"The market is full of AI that optimizes how often you contact a customer. The issuers winning right now use AI to decide how — and that's a behavioral science question."

The Science Behind Why People Actually Pay

Delinquency isn't purely a financial event. It's a behavioral one. Timing, channel, message framing, and emotional tone all measurably influence whether a past-due customer engages. A message that triggers shame or anxiety tends to produce avoidance. A message that offers a clear, low-friction path to resolution tends to produce the opposite.

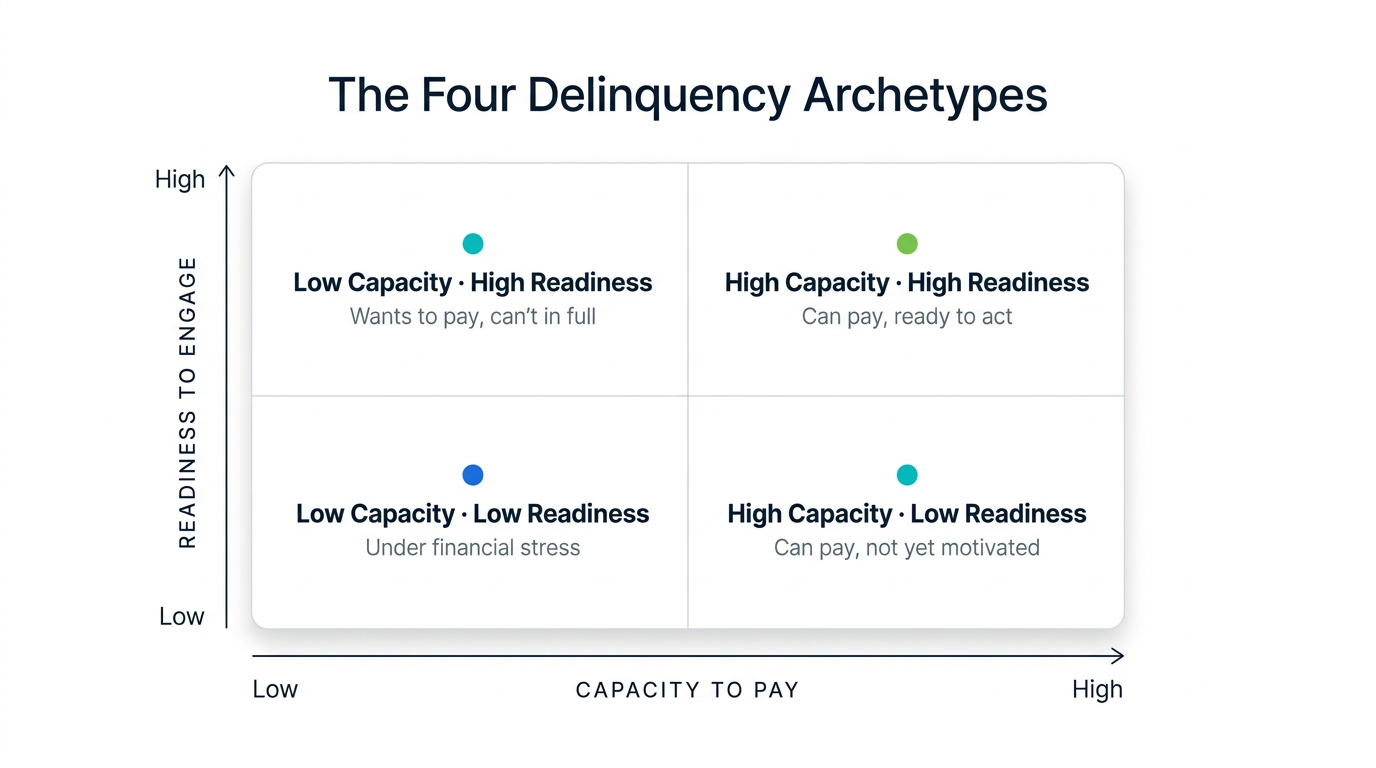

Symend's four delinquency archetypes formalize what behavioral science has established — that the barriers to payment differ fundamentally by customer type:

- HCHR (High Capacity, High Readiness): Can pay and wants to resolve. Needs a fast, frictionless path.

- HCLR (High Capacity, Low Readiness): Can pay but isn't motivated. Needs behavioral triggers that create urgency without pressure.

- LCHR (Low Capacity, High Readiness): Wants to pay but genuinely can't in full. Needs flexible options and supportive framing.

- LCLR (Low Capacity, Low Readiness): Under significant financial stress. Needs early, empathetic intervention — not escalation.

Symend segments past-due customers by capacity to pay and readiness to engage — not just days past due.

A collections strategy that can't distinguish between these four types can't treat any of them well. This is the difference between AI as a dialer and AI as a decision intelligence layer. The former optimizes contact rates. The latter — grounded in behavioral science — optimizes outcomes.

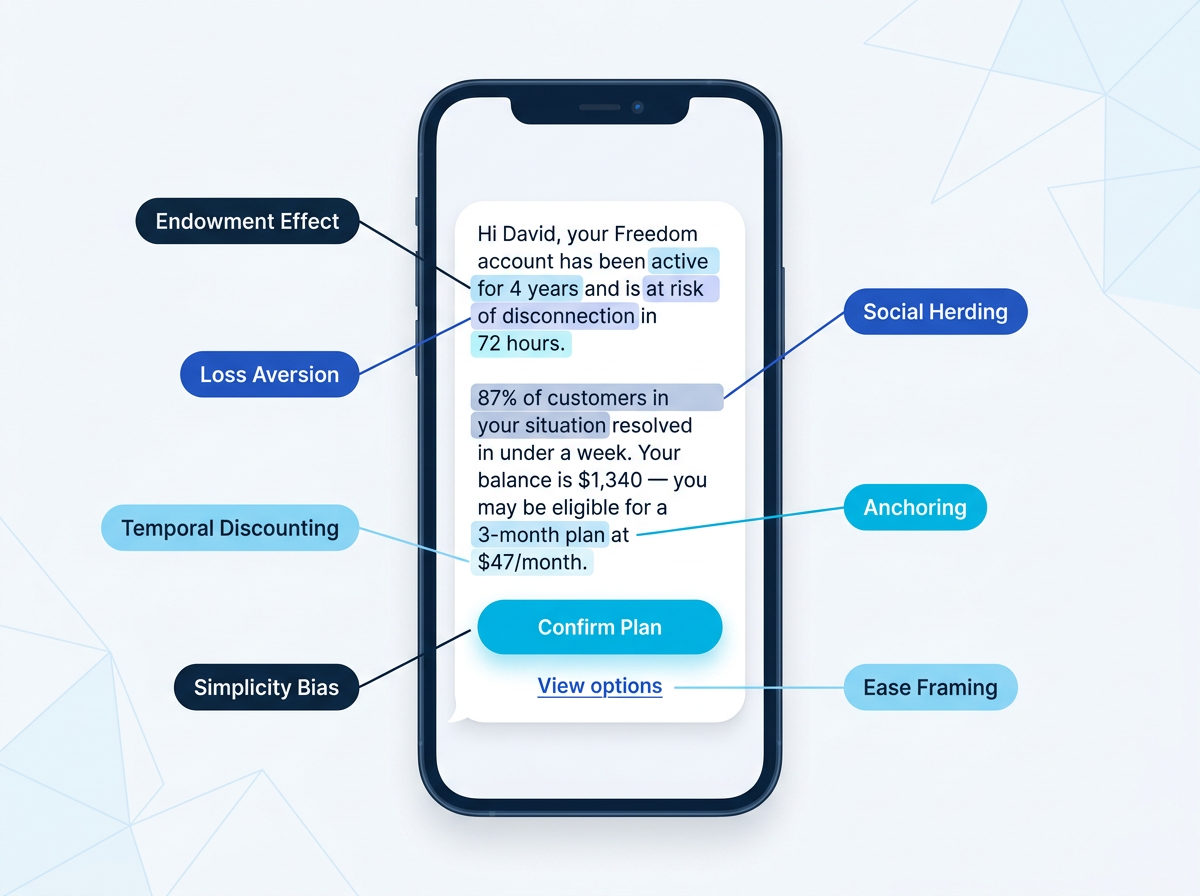

Archetype-level segmentation answers who to treat differently. The companion question is how — the specific behavioral tactics that determine whether a single message moves a customer to act. Loss aversion, anchoring, social herding, ease framing and four others all work on a past-due cardholder at the same time:

A single SMS doing the work of seven tactics. For a full breakdown, see 7 Behavioral Science Tactics That Determine Whether a Customer Pays.

SymendCure is built on this foundation: behavioral segmentation, Symend Scores derived from 100+ behavioral signals, and AI-optimized engagement flows that adjust continuously based on real-time customer behavior. It's the engine behind a documented 10x ROI across enterprise portfolios.

Case Study: How a UK Credit Card Provider Lifted Cure Rates 60%

A leading UK credit card provider faced exactly the pressure now bearing down on the broader market: rising delinquency, mounting cost-to-collect, and a traditional one-size-fits-all model that was failing to engage customers.

Working with Symend, the provider replaced blanket outreach with AI-powered behavioral segmentation — using 12 distinct archetypes that predict how each customer will respond to different engagement strategies, then tailoring message, channel, and timing to each one.

The results reframed what "good" looks like in card collections:

| Metric | Result |

|---|---|

| Cure rate lift | +60% |

| Reduction in outbound calls | −83% |

| Collected through digital engagement | £40M |

| Direct call center savings | £160K |

As the provider's Head of Collections Strategy put it, the behavioral approach changed how the team thinks about collections altogether — moving from treating every customer the same to understanding the underlying motivations and engaging in ways that actually work. The full story is in the UK credit card provider case study.

It's not an isolated win. One of North America's largest banks used the same behavioral approach to save $25M+, lifting cure rates and avoiding $24M in churn at an 11x ROI across consumer and small business portfolios — detailed in the major bank case study.

Beyond Recovery: Preventing the Next Delinquency

Here's what most collections strategies miss. Curing an account ends the immediate problem — but it does nothing about the household fragility that caused it. With delinquency rates at 15-year highs and consumers reporting the highest probability of missing a payment since the pandemic, a customer you cured this quarter is a strong candidate to fall behind again next quarter.

SymendPrevent closes that loop. It's a Bill Payment Protection solution offered to customers after they cure — at the precise moment financial awareness is heightened and they're most motivated to protect themselves. If a covered customer later experiences job loss, illness, disability, or death, their bills are covered for up to six months.

The behavioral logic is the point. Offering protection right after the stress of delinquency taps into a customer's heightened sensitivity to risk, which is what drives uptake. For the issuer, the effect is threefold: it directly offsets future bad debt through claims payouts, it reduces churn by embedding protection into the relationship, and it generates a new revenue stream through a commercial partnership model. Underwriting and claims are handled by major insurers, and Symend manages the entire customer journey — outreach, enrollment, payments, and support — so it lands as zero cost, zero risk, and zero IT lift.

In other words: collections done right isn't just about recovering a balance. It's about keeping the customer — and making the relationship more resilient than it was before they fell behind.

Five Shifts Card Issuers Need to Make Now

- Move intervention upstream. By the time an account is 60+ days past due, resolution cost and complexity have multiplied. Low-friction outreach at 15–30 days dramatically improves cure rates and cuts escalation costs.

- Segment by behavior, not just days past due. DPD tells you how long a problem has existed — not why, or what to do about it. Behavioral segmentation distinguishing capacity from readiness is the foundation of any strategy that performs across a diverse cardholder base.

- Engineer self-cure. A meaningful share of past-due customers will resolve independently given the right message, channel, and a friction-free payment path. Self-cure isn't passive — you design it.

- Make AI human-centered. AI should determine how you engage, not just how often. Use behavioral signals to inform framing, channel, and timing — not just to rank accounts by recovery probability.

- Close the loop with prevention. The cheapest delinquency to resolve is the one that never happens. Pair recovery with protection so cured customers don't simply re-enter the funnel next quarter.

The Path Forward for Card Issuers

The cardholders driving today's delinquency numbers aren't bad actors. They're people caught in a structural affordability squeeze — across the US, Canada, and the UK alike. Many want to pay. Many will, with the right engagement.

A UK provider proved what's possible: a 60% cure rate lift and 83% fewer outbound calls. A major bank saved more than $25M. And the issuers pairing behavioral recovery with prevention are building portfolios that don't just recover faster — they hold together better. That's not an anomaly. It's the blueprint.

See how behavioral science transforms card collections

Explore engagement built for today's credit card delinquency reality — recovery that preserves the relationship, and prevention that protects it. Request a custom ROI report or book a 15-minute demo.

FINANCIAL SERVICES SOLUTION REQUEST A DEMO